The currencies of Ghana and Zambia are coming under renewed pressure against the U.S. dollar, signaling a shift in momentum after both the Ghanaian cedi and Zambian kwacha posted strong performances earlier in 2026. Analysts now point to rising corporate demand for foreign exchange and fluctuations in global commodity markets as key drivers behind the recent depreciation trends.

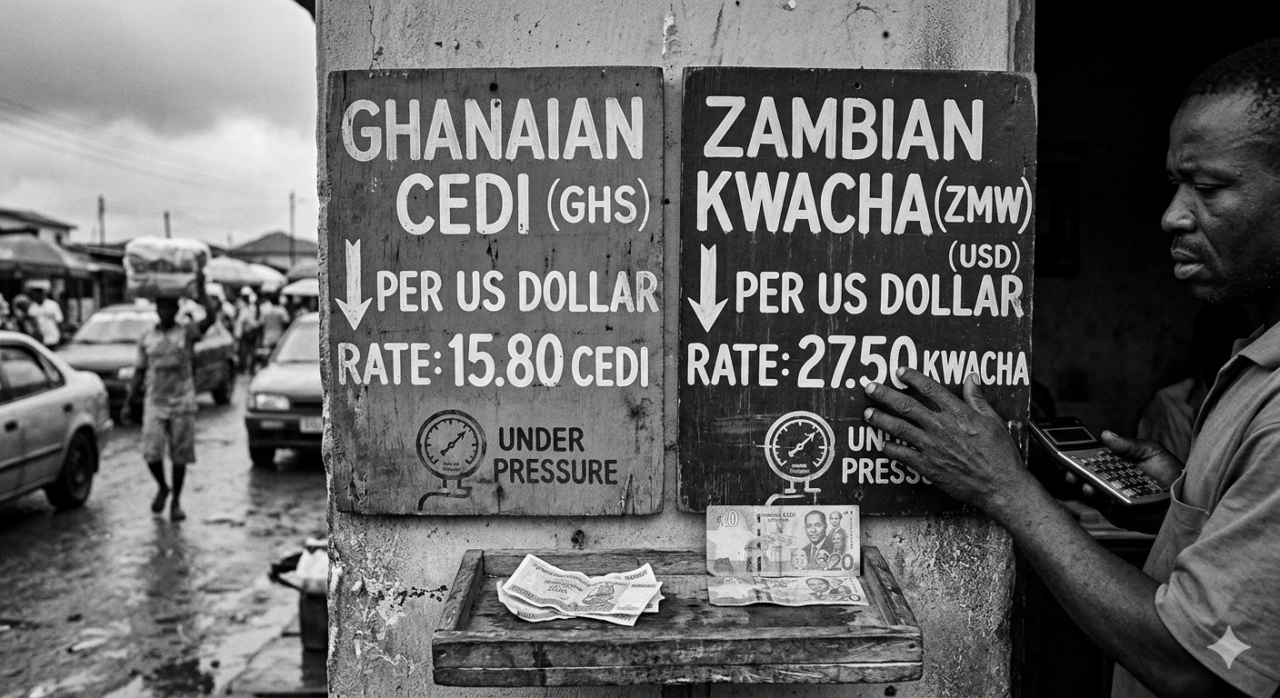

In Ghana, the cedi is extending a gradual decline as demand for foreign currency intensifies across major sectors of the economy. Businesses in energy, manufacturing, and commerce are increasingly seeking dollars to meet import obligations, placing sustained pressure on the local currency. As of April 16, the cedi was trading at approximately GH¢11.03 to GH¢11.05 on the interbank market, reflecting relative stability at the official level but underlying demand pressures beneath the surface.

At the retail level, however, the gap is more pronounced. Foreign exchange bureaus are quoting higher selling rates, with the dollar reaching as much as GH¢11.85. This spread between official and retail markets highlights liquidity constraints and localized demand imbalances, which can amplify perceptions of currency weakness among businesses and consumers.

In response to the economic pressures, the Ghanaian government has introduced temporary austerity measures aimed at cushioning the impact of rising fuel costs and currency depreciation. Announced on April 15, the measures include a subsidy of GHS 2.00 per liter on diesel to ease transportation and production costs, as well as a ban on fuel allowances for senior government officials. These steps are intended to reduce inflationary pressures while demonstrating fiscal discipline in a challenging economic environment.

Meanwhile, in Zambia, the kwacha is also facing headwinds after being widely recognized as the world’s best-performing currency earlier in the year. As of April 16, the kwacha was trading in the range of 19.13 to 19.40 per U.S. dollar, reflecting increased volatility and a weakening trend compared to its earlier gains.

A major factor behind the kwacha’s vulnerability is Zambia’s heavy reliance on copper exports, which account for more than 70 percent of the country’s foreign exchange earnings. Recent instability in global copper prices has reduced export revenue expectations, weakening the currency’s support base and exposing it to external shocks. As commodity markets fluctuate, the kwacha’s performance remains closely tied to global demand for copper.

In an effort to manage domestic liquidity and support economic activity, the Bank of Zambia recently reduced its Monetary Policy Rate to 13.5 percent. While this move is intended to stimulate growth and ease borrowing conditions, it may also contribute to short-term currency pressure by increasing money supply and reducing returns on local assets.

Zambia is also navigating a significant currency transition. The official exchange period for old banknotes ended on March 31, 2026, with the previous series ceasing to be legal tender in April. While such transitions are designed to improve monetary control and modernize currency systems, they can temporarily affect liquidity and market confidence during the adjustment period.

The parallel pressures facing both the cedi and the kwacha highlight the broader challenges confronting African economies in a volatile global environment. External factors such as commodity price swings, coupled with internal demand for foreign exchange, continue to shape currency performance. While both countries have implemented policy responses to stabilize their economies, maintaining currency strength will depend on sustained inflows, disciplined fiscal management, and improved resilience to global market fluctuations.

Source: Omanghana